Option Pricing

OVERVIEW

Successful options trading requires more than simply selecting a stock and arbitrarily choosing a strike price. Evaluating option pricing is a critical step in identifying trades with favorable risk-to-reward characteristics. Key metrics such as Delta, Implied Volatility (IV), and Open Interest provide valuable insight into the probability of success and overall trade quality.

Many successful option traders view Delta, Implied Volatility, and Open Interest as three essential components of trade evaluation: Delta helps assess probability, Implied Volatility helps determine option value, and Open Interest helps measure liquidity and market participation.

DELTA

DELTA helps traders estimate how much an option’s price may change relative to movements in the underlying stock while also providing an approximation of the option’s probability of expiring in-the-money. Specifically, Delta estimates how much an option’s value is expected to increase or decrease for every $1 move in the underlying security.

When evaluating potential trades, if you are buying calls, higher delta options generally offer a greater probability of success, while lower delta options provide increased leverage at the expense of lower probabilities. While not exact, these estimates can help traders align trade selection with their desired risk tolerance and probability objectives. Delta is often used as a quick estimate of the likelihood of success. The values below provide a rough estimate of the in-the-money success of the strike price chosen.

- 0.20 Delta ≈ 20% probability

- 0.30 Delta ≈ 30% probability

- 0.50 Delta ≈ 50% probability

- 0.70 Delta ≈ 70% probability

TRADING NOTE: If you are selling PUT options as your strategy, then a 0.20 Delta means there is an 80% chance that the strike price you have chosen will not be reached and the PUT will expire worthless and thus your profit is the premium collected for the cost of the PUT. Another example, if your Delta is 0.05 then your odds of keeping the premium is 95%. You can simply sort Delta, pick out Delta’s that are 0.05 or lower and your chances of success at those prices is about 95%.

IMPLIED VOLATILITY

Measures the market’s expectations for future price movement and can help determine whether options are relatively expensive or inexpensive compared to historical levels. As implied volatility rises, option premiums generally increase due to the greater likelihood of significant price fluctuations.

Conversely, lower implied volatility typically results in less expensive option premiums. Traders use implied volatility to evaluate whether options are relatively expensive or inexpensive and to select strategies that align with market conditions. High implied volatility environments often favor premium-selling strategies, while low implied volatility environments may create opportunities for premium-buying strategies.

TRADING NOTE: High implied volatility environments often favor premium-selling strategies because option prices are elevated, while low implied volatility environments may create opportunities for premium-buying strategies. As a practical rule,”Buy options when implied volatility is low and likely to rise; sell options when implied volatility is high and likely to fall.”

OPEN INTEREST

Represents the total number of outstanding option contracts that have been opened but not yet closed, exercised, or expired. Traders use open interest to evaluate liquidity, market participation, and the strength of potential price movements. Higher open interest generally indicates greater trading activity and tighter bid-ask spreads, making it easier to enter and exit positions efficiently. In addition, traders analyze open interest at specific strike prices to identify potential support and resistance levels and to gain insight into market sentiment.

TRADING NOTE: Look for trades where the difference between the “BID” and the “ASK” price is relatively small (like within 10 cents). It is not always possible, but the shorter the distance between the BID price and the ASK price, means a better priced option for you. It is also a reflection of buyer and seller interest and liquidity levels. Higher liquidity means it is easier to enter and exit trades at favorable prices.

OPTION CHAIN

OVERVIEW

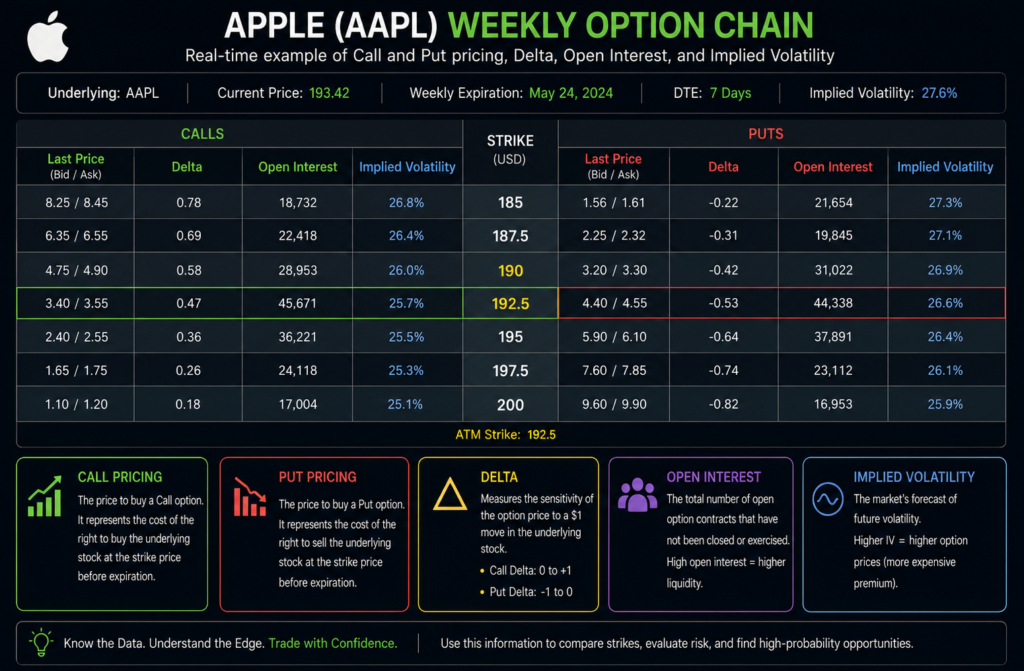

The CALL and PUT prices displayed on an “option chain” (example below) represent the premium required to purchase the rights associated with each option contract. The price listed is per share but you buy or sell puts in 100 share increments. For example, if you are selling 2 contracts (either Calls or Puts) then that transaction represents 200 shares. To calculate the premium, take the number of shares involved times the cost per share.

A CALL option premium reflects the market’s valuation of the right to buy the underlying stock at a specific strike price, while a PUT option premium reflects the value of the right to sell the stock at a specified strike price. These premiums are influenced by several factors, including the stock’s current price, strike price, time remaining until expiration, implied volatility, interest rates, and market demand.

CALL EXAMPLE

In the example below, for Apple Stock, at a strike price of $190, if you sold the CALL option the buyer would pay you $3.40 to $3.55 (about $3.47 as a mid point) for 100 shares for that option. You would receive in your account $347 ($3.47 X 100) as the premium. At the time of expiration (in this example, May 24th) if the price per share exceeded $190 then the buyer of the call option has the option, not the obligation, to purchase those 100 shares at $190 per share and you, as the seller of the option, must deliver to the buyer those shares at $190.

Lets say the price dropped to $185 per share by May 24th, then the buyer would not exercise his option to buy the shares at $190 since he could get them on the open market for $185 and you would walk away with the premium of $347 as this was paid to you by the buyer.

PUT EXAMPLE

If you sold a PUT option at a strike price of $190, then you would receive $325 (mid point between $330 and $320) as the premium. If by May 24th, the date the option expires, the price did not fall below $190 then you walk away with the premium. If the price dropped to $185, for example, then you are required to buy the stock from the PUT buyer for $190 per share. Many PUT buyers will buy PUTS as a hedge, to protect their capital investments.

TRADING NOTE: Studying the Option Chain is really very useful. The Open Interest column tells you what other traders are thinking and where they are placing their trades. You can sort each column and it always an interesting exercise to see where the majority of traders are placing their trading bets. You should also sort the Delta values as this information revealed in this column is very insightful.

SUMMARY

A useful way to think about an option chain is that it represents the market’s collective assessment of probability, risk, and expected future price movement, with the call and put premiums reflecting what traders are willing to pay for those opportunities.

By analyzing these factors together, you will make more informed decisions when selecting strike prices, improve your trade execution, and increase the likelihood of aligning each position with their specific strategy and risk tolerance. Understanding option pricing is not just a technical exercise—it is a foundational skill that can significantly enhance long-term trading performance. Remember, you are not being paid for the time spent trading rather you are rewarded for the quality of your decision making when making trades. Understanding these principles will enhance your judgement.